Opening your annual auto insurance renewal notice to find a significantly higher price tag is a universally frustrating experience. It is especially infuriating when you have spent the last 12 months being a perfect driver you haven’t had a single accident, you haven’t received a speeding ticket, and you haven’t filed a claim. Yet, the price continues to climb.

In the modern landscape of 2026, car insurance premiums are no longer calculated using simple, backward-looking metrics. The days of simply looking at your age, your car’s make, and your driving record are long gone. Today, auto insurance underwriting is driven by massive data centers, predictive analytics, artificial intelligence, and incredibly complex actuarial models that evaluate risk on a microscopic level.

Insurance companies now analyze dozens sometimes hundreds of interconnected data points to predict your individual risk level, forecast the specific cost of potential claims, and ensure the long-term profitability of their entire risk pool.

Understanding the exact mechanics of how car insurance premiums are calculated is the most powerful tool a consumer can wield. When you decode the algorithm, you stop guessing and start making strategic, informed decisions. This comprehensive master guide will pull back the curtain on the auto insurance industry in 2026, explaining precisely what factors matter most, why prices differ so drastically between drivers, and how you can manipulate these variables to secure the lowest possible rate.

Table of Contents

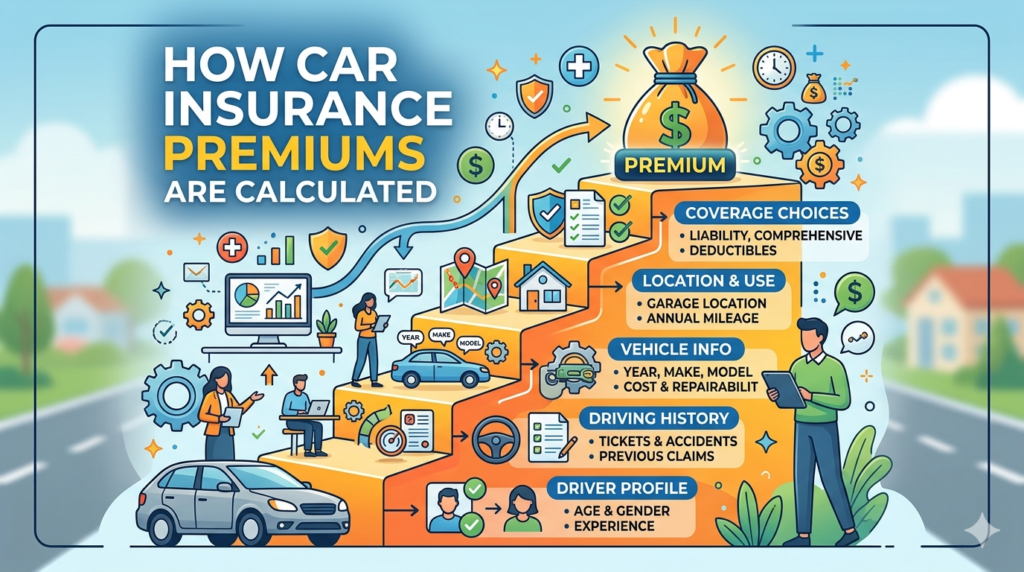

What Exactly is a Car Insurance Premium?

At its core, a car insurance premium is the financial cost of transferring your risk to a massive corporate entity. It is the specific amount of money you agree to pay an insurance carrier—whether monthly, semi-annually, or annually—to keep your financial protection active and in force.

However, a premium is not a random number pulled out of thin air. It is the result of a mathematical equation designed to balance out four critical pillars:

- Claim Probability: The statistical likelihood that you, specifically, will file a claim during the policy period.

- Severity Forecasting: The estimated financial cost of that claim if it actually happens (e.g., will you likely have a $500 fender bender or a $50,000 total loss?).

- Operational Overhead: The administrative costs required to run the insurance company, including employee salaries, office buildings, marketing, and legal defense teams.

- Regulatory and Market Conditions: State-mandated taxes, fees, and the overall macroeconomic climate (such as inflation and supply chain health).

Insurers use predictive data-driven models to balance this risk against their pricing. The goal of the insurance company is to collect enough premiums from the entire “pool” of safe drivers to pay for the devastating accidents of the risky drivers, while still generating a corporate profit margin.

The Algorithmic Shift: How Insurers Calculate Risk in 2026

To understand your premium, you must understand the concept of “Base Rates” and “Multipliers.”

Every insurance company starts by establishing a Base Rate for your state or region. This is the starting price for a hypothetical, perfectly average driver. From there, the underwriting algorithm applies a series of “Multipliers” (or rating factors) based on your unique profile.

- If a factor makes you less risky, the multiplier is less than 1.0 (e.g., a 0.8 multiplier creates a 20% discount).

- If a factor makes you more risky, the multiplier is greater than 1.0 (e.g., a 1.5 multiplier creates a 50% surcharge).

Higher calculated risk = Higher multiplier = Higher car insurance premiums. Lower calculated risk = Lower multiplier = Lower car insurance premiums.

This risk-based pricing approach is the absolute foundation of the industry. Let’s execute a deep dive into the 10 most critical factors that determine your final price.

Factor 1: Your Driving Record and Comprehensive Claims History

Your past behavior behind the wheel remains the single most heavily weighted factor in the entire underwriting equation. Insurers rely on the philosophy that past behavior is the most accurate predictor of future risk.

When you request a quote, the insurer pulls your Motor Vehicle Report (MVR) from the DMV and your C.L.U.E. Report (Comprehensive Loss Underwriting Exchange), which lists every insurance claim you have filed in the last five to seven years.

What the Algorithm Scrutinizes:

- At-Fault Accidents: Causing an accident proves you are a high-risk liability. A single at-fault accident can instantly spike your car insurance premiums by 30% to 50% for the next three to five years.

- Moving Violations: Speeding tickets, running red lights, and illegal turns indicate reckless tendencies.

- Major Infractions: A DUI (Driving Under the Influence) or a reckless driving conviction is the fastest way to ruin your insurance profile. Many standard carriers will drop you entirely, forcing you into the exorbitant “high-risk” (SR-22) insurance market.

- Not-At-Fault Claims: Even if an accident wasn’t your fault, or if you filed a comprehensive claim (like hail damage or a cracked windshield), filing too many of these claims flags you as a “frequent filer,” which can trigger rate increases.

Factor 2: Vehicle Type, Technology, and Repair Costs

The actual machine you drive dictates the severity of a potential claim. In 2026, not all cars cost the same to insure, and the logic goes far beyond the retail price of the vehicle.

Key Vehicle Factors Analyzed:

- Cost of Replacement Parts and Labor: A standard domestic sedan uses cheap, widely available parts. A luxury imported vehicle requires expensive parts shipped from overseas and specialized mechanics who charge higher hourly labor rates.

- Advanced Driver Assistance Systems (ADAS): While automatic braking and lane-keep assist systems prevent accidents, they make the car vastly more expensive to repair. A bumper with a LiDAR sensor and a rearview camera costs thousands of dollars more to replace than a traditional plastic bumper.

- Electric Vehicle (EV) Status: EVs often carry higher premiums due to the immense cost of replacing damaged lithium-ion battery packs, which can easily total a vehicle even after a relatively minor undercarriage strike.

- Historical Safety and Theft Ratings: The algorithm checks the national database for your specific make and model. If your car is a top target for organized auto theft rings, your comprehensive coverage premium will soar. Conversely, if your car has top-tier crash test ratings that protect occupants effectively, your bodily injury liability costs will decrease.

Factor 3: Location and Micro-ZIP Code Risk Profiling

In the insurance world, your physical address is a massive determinant of your financial liability. Auto insurance is hyper-local. When analyzing how car insurance premiums are calculated, where you park your car at night is just as important as how you drive it.

Location-Based Risk Variables:

- Traffic Density and Urbanization: Urban centers with congested intersections and bumper-to-bumper traffic inherently experience a drastically higher volume of daily fender-benders than rural farm towns. If you live in a city, you pay an urban density penalty.

- Local Crime Rates: Insurers cross-reference your specific ZIP code with local police data. High rates of vehicle theft, catalytic converter theft, and street vandalism will directly increase the cost of your comprehensive coverage.

- Regional Weather Vulnerability: If you live in a coastal area prone to hurricanes, a midwestern state famous for golf-ball-sized hail, or a region plagued by seasonal wildfires, your geographic exposure to “Acts of God” elevates your premium.

- Litigation Climate: Some states and counties are notoriously litigious, meaning drivers are highly likely to sue each other after minor accidents. Insurers charge more in these regions to cover anticipated legal defense costs.

Factor 4: Annual Mileage and Vehicle Usage Designation

The mathematical reality is simple: the more time your car spends on the road, the higher your exposure to a statistical accident. Insurers track how far you drive and why you are driving.

Usage Categories and Premium Impact:

- Pleasure Use: If you work from home and only drive a few thousand miles a year to buy groceries and visit friends, you represent the lowest possible risk and receive the lowest rates.

- Daily Commuting: Driving in heavy rush-hour traffic five days a week significantly elevates your risk profile. The longer your daily commute in miles, the higher your base rate will climb.

- Business or Commercial Use: If you use your personal vehicle to deliver pizzas, drive for rideshare apps (like Uber or Lyft), or transport heavy business equipment, standard personal policies will not cover you. You require commercial-grade endorsements, which carry significantly higher car insurance premiums due to the extended liability exposure.

Factor 5: Credit-Based Insurance Scores (The Hidden Metric)

One of the most controversial, yet impactful, methods of how car insurance premiums are calculated in 2026 is the use of your financial credit history. In states where it is legally permitted, insurers generate a “Credit-Based Insurance Score.”

Why Financial History Matters to Auto Insurers: Decades of intensive actuarial data have proven a stark, undeniable correlation between a person’s credit management and their likelihood to file an insurance claim. Statistically, individuals with lower credit scores file more frequent, and more expensive, auto insurance claims than those with excellent credit.

How It Affects Your Bottom Line: Your credit-based insurance score does not look at your income; it looks at your reliability. It tracks your outstanding debt ratio, your history of late payments, and bankruptcies.

- Drivers with Excellent Credit receive the best baseline multipliers and massive discounts.

- Drivers with Poor Credit can actually pay more for auto insurance than a driver with a clean credit history who has a prior DUI conviction. (Note: A few states, including California, Hawaii, and Massachusetts, have legally banned insurers from using credit scores to determine auto rates).

Factor 6: Age, Driving Experience, and Demographic Profiling

Insurance pricing is fundamentally prejudiced based on statistical group behavior. Until you have established a long personal driving history, you are judged by the actions of your demographic peers.

The Demographic Risk Brackets:

- The Youth Penalty (Under 25): Teenage drivers and young adults under 25 are statistically the most dangerous drivers on the road. They lack experience, have slower hazard recognition, and are highly prone to distracted driving. Adding a 16-year-old to a family policy can easily double the overall premium.

- The Prime Years (30 to 65): These drivers enjoy the lowest premiums. They have decades of experience, stabilized life routines, and statistically cause the fewest catastrophic accidents.

- Senior Drivers (70+): As drivers age into their 70s and 80s, premiums begin to slowly creep up again. Slower reflex times, degraded night vision, and the physical fragility of older drivers (making injuries more severe in minor crashes) increase the underwriting risk.

- Marital Status: Statistically, married individuals are involved in fewer accidents than single individuals. Insurers view marriage as a sign of stability, routinely offering lower rates to married couples.

Factor 7: Coverage Limits, Deductibles, and Policy Architecture

You have direct control over this factor. The specific structure of the policy you build actively dictates the final price of the premium. You get what you pay for.

The Levers of Policy Pricing:

- Liability Limits: Buying the state minimum liability limits (e.g., $25,000 to cover another person’s injuries) is cheap but dangerous. Opting for robust, expert-recommended limits (e.g., $250,000 per person / $500,000 per accident) requires the insurer to take on massive financial risk, thereby raising your premium.

- The Deductible Seesaw: Your deductible is the amount of money you agree to pay out of your own pocket before the insurance kicks in to repair your car.

- Low Deductible ($250): High monthly premium. The insurer knows you might file a claim for a minor door ding.

- High Deductible ($1,000+): Low monthly premium. The insurer knows you will handle minor damages yourself and only rely on them for major catastrophes.

- Optional Endorsements: Adding luxuries like Roadside Assistance, Rental Car Reimbursement, and Gap Insurance will incrementally increase your total monthly cost.

Factor 8: Insurance History and Coverage Continuity

Insurance companies fiercely value stability and loyalty. Your track record as a consumer plays a subtle but vital role in your final price quote.

Red Flags the Algorithm Looks For:

- Lapses in Coverage: If you let your insurance expire for even one day (perhaps you forgot to pay the bill or were between vehicles), you are immediately reclassified as a “High-Risk Driver.” A gap in coverage proves irresponsibility to the algorithm, resulting in harsh premium penalties.

- Prior Liability Limits: When you switch to a new insurer, they look at the policy you are leaving. If you currently carry high liability limits, the new insurer views you as a responsible asset protector and offers better rates. If you carry state minimums, you are viewed as a baseline risk.

- Consistent Payment History: Setting up automatic payments via electronic funds transfer (EFT) or paying your 6-month premium entirely in full upfront usually secures an immediate administrative discount.

Factor 9: Macro-Market Conditions and Industry Claim Trends

Sometimes, your premium increases through absolutely no fault of your own. You are subject to the macroeconomic winds blowing through the global economy in 2026.

Industry-Wide Influences:

- Inflationary Pressures: When the cost of steel, microchips, and automotive paint rises, the cost of paying out claims rises. Insurers proactively raise base rates to ensure they have enough capital to afford tomorrow’s inflated repair bills.

- Social Inflation: Juries are increasingly awarding massive, multi-million-dollar settlements to accident victims. To afford these “nuclear verdicts” and the associated legal defense fees, insurers spread the cost across all policyholders.

- Supply Chain Disruptions: When parts are scarce, cars sit in repair shops for months waiting for components. Because the insurer has to pay for your rental car for those entire two months, the total cost of the claim skyrockets, leading to industry-wide rate adjustments.

Factor 10: Insurer-Specific Proprietary Pricing Models

Finally, it is essential to understand that there is no universal pricing manual. Every single insurance company utilizes a different, highly secretive proprietary algorithm.

Why Car Insurance Quotes Vary So Wildly:

- Target Demographics: Company A might want to insure safe, middle-aged suburban families driving minivans, offering them unbeatable rates. Company B might specialize in insuring high-risk young drivers with sports cars.

- Loss Ratios by Region: If Company A suffered massive financial losses due to a massive hailstorm in your specific ZIP code last year, they will aggressively raise rates in your area to recover capital. Company B, which didn’t have many customers in that ZIP code, will keep their rates low.

- Price Optimization Algorithms: Some insurers use Big Data to calculate exactly how much they can raise your rates at renewal before you get angry enough to leave. This is why loyalty is often penalized in the insurance industry.

This proprietary variation is precisely why comparing quotes across multiple carriers is the only way to find the true market value of your profile.

Proactive Defense: How Drivers Can Positively Influence Their Premiums

While you cannot change your age or fix global inflation, you hold the power to manipulate several key variables within the algorithm. Use these smart strategies to force your car insurance premiums downward:

- Defend Your Driving Record: Drive defensively. Utilize your car’s ADAS features. Avoiding a single at-fault accident is worth thousands of dollars in premium savings over a three-year period.

- Optimize Your Credit Health: Pay down high-interest credit card balances and ensure your bills are paid on time. Elevating your credit score from “Fair” to “Excellent” can slash your auto insurance bill by over 20% in many states.

- Leverage Telematics (Usage-Based Insurance): If you are a genuinely safe driver, prove it to the algorithm. Download your insurer’s telematics app to track your driving. If you avoid hard braking, rapid acceleration, and late-night driving, you can earn up to a 30% permanent discount based on your actual behavior, rather than demographic assumptions.

- Ruthlessly Compare Quotes Annually: Never let your policy auto-renew without checking the market. Because proprietary algorithms change constantly, the company that was the cheapest for you three years ago is rarely the cheapest for you today.

- Master the Art of Bundling: Combine your auto insurance with your homeowner’s or renter’s insurance under the same carrier. This creates “account density,” making you a highly profitable client, which unlocks the largest single discount available in the industry (often 15% to 25%).

Frequently Asked Questions (FAQ)

Why did my car insurance premium increase when I haven’t had an accident in 10 years?

Your personal driving record is only one piece of the puzzle. If the cost to repair vehicles in your state has surged due to inflation, or if your specific region experienced an abnormal amount of severe weather claims (floods, hail), the insurance company will raise the base rate for everyone in that geographic risk pool to remain financially solvent.

Do car insurance premiums automatically decrease as my car gets older?

Not necessarily. While the actual cash value of your vehicle drops (which can slightly lower your collision coverage cost), the cost to repair the vehicle—labor rates, paint, and replacement parts—continues to rise with inflation. Furthermore, liability costs (paying for the damage you do to others) never decrease just because your car is older.

How often do insurance companies recalculate my premium?

Premiums are officially recalculated at the end of every policy term (typically every 6 or 12 months) during the renewal phase. However, midterm adjustments can occur if you trigger a material change: moving to a new address, buying a new car, adding a teenage driver, or modifying your coverage limits.

Is it true that the color of my car affects how my premium is calculated?

No, this is one of the oldest myths in the automotive world. Insurance algorithms do not factor in the color of your paint. Whether you drive a fire-engine red sports car or a beige minivan, the underwriter only cares about the vehicle’s engine size, historical crash statistics, and theft data.

Can checking my credit score frequently hurt my insurance rates?

No. When an insurance company checks your credit to formulate a quote, they perform a “soft pull” or “soft inquiry.” Unlike applying for a mortgage or a new credit card (which is a “hard pull”), soft inquiries have absolutely zero negative impact on your FICO credit score, no matter how many insurance companies you request quotes from.

Conclusion: Empowering Yourself Through Knowledge

In 2026, the mechanics behind how car insurance premiums are calculated represent a triumph of complex predictive analytics and massive data processing. Insurance carriers leave absolutely nothing to chance, evaluating every facet of your demographic profile, vehicle specifications, financial habits, and geographic environment to assign you a highly specific financial risk score.

While this system can feel opaque and occasionally unfair, understanding the exact rules of the game is the ultimate consumer advantage. By recognizing which factors carry the heaviest mathematical weight, you can actively optimize your risk profile.

The best way to control your car insurance premiums is not by making blind guesses or relying on corporate loyalty. It is achieved through active management: keeping your driving record pristine, elevating your credit health, adjusting deductibles strategically, and aggressively leveraging the open market to compare car insurance quotes every single year. When you understand the numbers behind the algorithm, you stop being a passive consumer and start protecting your wealth.

Sources

- Insurance Information Institute – What Determines Auto Insurance Pricing

- Consumer Financial Protection Bureau – Auto Insurance Rate Factors