As healthcare costs continue to skyrocket across the globe in 2026, choosing the right medical coverage strategy is no longer just a routine administrative task—it has become one of the most critical financial decisions you will make for your household. The era of simply checking a box during your employer’s open enrollment period and hoping for the best is over. Today, a miscalculation in your healthcare strategy can result in thousands of dollars in wasted premiums or crippling out-of-pocket medical debt.

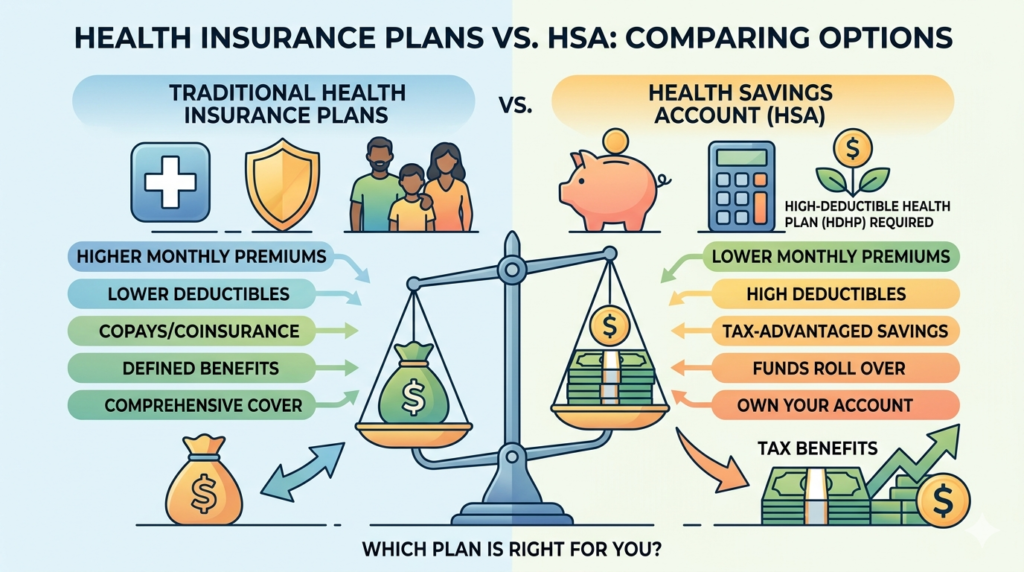

Millions of individuals and families now find themselves staring at a complex crossroads, forced to choose between the predictable safety of Traditional Health Insurance Plans and the wealth-building, tax-advantaged power of pairing a high-deductible plan with a Health Savings Account (HSA).

While these two options serve fundamentally different primary purposes—one transfers immediate risk to an insurance company, while the other empowers you to build a personal medical treasury—they are not inherently at odds. In fact, understanding how they contrast, intersect, and work together is the absolute key to controlling your medical expenses while simultaneously bulletproofing your long-term financial independence.

As a senior financial and insurance analyst, I have designed this comprehensive, 3,000-word master guide to demystify the healthcare landscape of 2026. We will dissect the architecture of traditional health plans, reveal the staggering financial power of the HSA, run real-world mathematical cost comparisons, and provide you with an actionable blueprint to choose the exact coverage strategy that fits your medical needs and your budget.

Table of Contents

Part 1: The Architecture of Traditional Health Insurance Plans

Before we can compare strategies, we must establish a firm understanding of traditional coverage. At its core, a health insurance plan is a financial risk-transfer contract. You agree to pay a set amount of money (a premium) to an insurance carrier, and in exchange, the carrier agrees to absorb the catastrophic financial risk of your medical care, negotiating lower rates with doctors and hospitals on your behalf.

What Do Traditional Health Plans Typically Cover?

Under current 2026 healthcare regulations, fully compliant traditional health insurance plans are legally required to provide comprehensive coverage across several essential health benefit categories. These include:

- Preventive and Wellness Care: This is arguably the most valuable immediate benefit. Annual physicals, standard bloodwork, vital cancer screenings (like mammograms and colonoscopies), and pediatric immunizations are covered at 100%. You pay absolutely nothing out-of-pocket for these services, even if you haven’t met your deductible.

- Ambulatory Patient Services: Outpatient care, routine doctor consultations, and specialist visits.

- Hospitalization and Surgeries: Coverage for overnight hospital stays, emergency room visits, complex surgical procedures, and facility fees.

- Prescription Medications: Access to a tiered formulary that covers generic, preferred brand-name, and specialty biological drugs.

- Maternity and Newborn Care: Comprehensive coverage for prenatal visits, labor, delivery, and postpartum care.

- Mental Health and Substance Abuse Services: Inpatient and outpatient behavioral health treatment.

By sharing the cost of these expensive services between you and the massive risk pool managed by the insurer, traditional health insurance plans prevent a single diagnosis from resulting in personal bankruptcy.

The Financial Levers: Decoding the Jargon

To understand how much traditional plans actually cost, you must master the four financial levers that dictate your out-of-pocket exposure:

- The Premium: The non-refundable monthly subscription fee you pay just to keep the policy active.

- The Deductible: The threshold amount you must pay entirely out of your own pocket for medical services before the insurance company begins to share the costs. (Note: Preventive care bypasses the deductible).

- Copayments (Copays): A flat, predictable fee (e.g., $30) you pay at the reception desk for specific routine services, like a visit to a specialist or a prescription refill.

- Coinsurance: Once your deductible is met, coinsurance is the percentage split of the remaining bill. If you have 20% coinsurance, you pay 20% of the MRI cost, and the insurer pays 80%.

- The Out-of-Pocket Maximum (OOP Max): Your absolute financial ceiling. Once your deductibles, copays, and coinsurance payments hit this legal limit for the year, the insurance company takes over and pays 100% of all covered medical costs.

Part 2: The Four Pillars of Traditional Health Plan Networks

Traditional health insurance plans are not monoliths. They are divided into distinct network architectures, each balancing your freedom to choose your doctor against the cost of your monthly premium.

1. HMO (Health Maintenance Organization)

The HMO is the strictest, most highly managed care model available, designed to keep premium costs as low as possible.

- How it Works: You are required to select a Primary Care Physician (PCP) who acts as the “gatekeeper” to the healthcare system. If you want to see a dermatologist for a rash, you cannot simply call the dermatologist. You must visit your PCP first, pay a copay, and obtain an official, approved referral to the specialist.

- The Network Rule: With the rare exception of a true, life-threatening emergency, an HMO will pay absolutely $0 if you receive care from an “out-of-network” doctor or facility. You are strictly confined to their local ecosystem.

- Best For: Budget-conscious individuals and healthy families who want lower premiums, predictable flat-fee copays, and who do not mind navigating bureaucratic referrals.

2. PPO (Preferred Provider Organization)

The PPO is the gold standard for medical freedom, making it highly popular, but also the most expensive traditional option.

- How it Works: You have ultimate autonomy. You do not need to designate a primary care physician, and you never need a referral to see a specialist. If your knee hurts, you can instantly book an appointment with a top-tier orthopedic surgeon.

- The Network Rule: PPOs offer extensive out-of-network benefits. If you choose to see a doctor who is not contracted with the insurer, the PPO will still pay a portion of the bill (though your coinsurance rate will be noticeably higher than if you stayed in-network).

- Best For: Individuals with complex chronic conditions, people who travel frequently out of state, and anyone willing to pay a premium surcharge for absolute control over their medical care.

3. EPO (Exclusive Provider Organization)

An EPO is a modern hybrid that attempts to blend the cost-savings of an HMO with the administrative ease of a PPO.

- How it Works: Like a PPO, you are not forced to select a primary care physician, and you do not need referrals to see in-network specialists. You have administrative freedom.

- The Network Rule: Like an HMO, the network boundary is a brick wall. If you go out-of-network for non-emergency care, you are responsible for 100% of the massive medical bill.

- Best For: Consumers who hate dealing with PCP referrals but are perfectly content staying within a specific, localized network of high-quality doctors and hospitals to save money on premiums.

4. POS (Point of Service)

A POS plan is a less common blend that leans heavily on HMO rules but offers a small safety valve.

- How it Works: You must select a primary care physician and obtain referrals for specialist care.

- The Network Rule: Unlike an HMO, a POS plan will provide partial coverage if you go out-of-network, but the out-of-pocket costs will be aggressively high.

- Best For: Individuals who want the guided care of an HMO but want the peace of mind knowing they can occasionally step out of the network if absolutely necessary.

Part 3: The High-Deductible Health Plan (HDHP) Revolution

To understand the Health Savings Account (HSA), you must first understand the vehicle required to unlock it: The High-Deductible Health Plan (HDHP).

In the early 2000s, the government realized that traditional, low-deductible insurance plans (where people paid a simple $20 copay for everything) were masking the true, hyper-inflated cost of healthcare from consumers. To incentivize patients to become smarter shoppers and care more about the cost of medical services, the HDHP was born.

An HDHP operates on a drastically different financial philosophy than a traditional PPO or HMO.

- The Premium: HDHPs feature significantly lower monthly premiums. Because you are agreeing to take on more upfront risk, the insurance company gives you a massive discount on your monthly bill.

- The Deductible: You are responsible for a much larger initial chunk of your medical bills. In an HDHP, there are usually no flat-fee copays for doctor visits or prescriptions. If an MRI costs $1,000, you pay the full $1,000 negotiated rate until you hit your massive deductible (which is often $3,000 to $5,000+).

- The Exception: Just like traditional plans, HDHPs still cover all legally mandated preventive care (annual physicals, vaccines, screenings) at 100% before the deductible is met.

Because the government recognizes that forcing you to pay a $4,000 deductible out of pocket is financially painful, they created a powerful, tax-sheltered financial tool to help you pay for it: The Health Savings Account.

Part 4: Mastering the Health Savings Account (HSA)

A Health Savings Account (HSA) is not an insurance plan. It is a specialized, private financial account—similar to a 401(k) or an IRA—that you own and control. It is designed specifically to help you save and invest money to pay for qualified medical expenses.

Critical Rule: You are legally prohibited from opening or contributing to an HSA unless you are actively enrolled in a qualifying High-Deductible Health Plan (HDHP).

The “Triple Tax Advantage” (The Holy Grail of Finance)

Financial advisors, CPAs, and wealth managers in 2026 unilaterally consider the HSA to be the most powerful tax-advantaged account in the entire United States tax code. It is the only account that offers the legendary “Triple Tax Advantage”:

- Tax-Deductible Contributions (Money Going In): Every dollar you deposit into your HSA reduces your taxable income for the year. If you make $80,000 a year and contribute $4,000 to your HSA, the IRS only taxes you as if you made $76,000. If your employer deducts the contribution directly from your paycheck, it bypasses payroll taxes (FICA) entirely, saving you an additional 7.65% immediately.

- Tax-Free Growth (Money Expanding): Your HSA is not just a standard checking account. You can actively invest your HSA funds into the stock market (mutual funds, index funds, ETFs, and stocks). As your investments grow and compound over decades, you pay absolutely zero taxes on the capital gains or dividends.

- Tax-Free Withdrawals (Money Coming Out): As long as you use the money to pay for a “Qualified Medical Expense,” the withdrawal is 100% tax-free. You never pay taxes on that money, ever.

2026 HSA Contribution Limits

The IRS strictly regulates how much capital you can shelter inside this powerful account. For the 2026 tax year, the contribution limits have increased to adjust for inflation:

- Individual Coverage: You can contribute up to $4,300 per year.

- Family Coverage: You can contribute up to $8,550 per year.

- Catch-Up Contribution: If you are age 55 or older, the IRS allows you to contribute an additional $1,000 per year to accelerate your savings before retirement.

What Constitutes a “Qualified Medical Expense”?

The IRS is surprisingly generous regarding what you can buy with your tax-free HSA funds. Qualified expenses include:

- Deductibles, copays, and coinsurance payments.

- Prescription medications and over-the-counter (OTC) drugs (like Tylenol, allergy meds, and cold medicine).

- Dental treatments, cleanings, braces, and extractions.

- Vision care, including eye exams, prescription glasses, contact lenses, and even Lasik eye surgery.

- Mental health counseling and psychiatric care.

- Medical equipment, wheelchairs, hearing aids, and CPAP machines.

- Note: You cannot use HSA funds to pay your actual monthly insurance premiums (with a few rare exceptions, like COBRA or Medicare premiums).

The Hidden Superpower: The Stealth Retirement Account

Here is the secret that makes the HSA so incredibly popular in 2026: The funds never expire. Unlike a Flexible Spending Account (FSA), which forces a “use it or lose it” rule at the end of the year, your HSA balance rolls over indefinitely, year after year, decade after decade. It belongs to you, not your employer. If you change jobs, the HSA comes with you.

Because the funds roll over and can be invested in the S&P 500, healthy individuals use the HSA as a “Stealth Retirement Account.” They max out their HSA contributions every year, pay for their minor medical expenses out-of-pocket using their regular checking account, and leave the HSA untouched to compound in the stock market for 30 years.

Furthermore, once you turn age 65, the rules change. At 65, you can withdraw money from your HSA for any non-medical reason (like buying a boat or taking a vacation) without paying the standard 20% IRS penalty. You will simply pay normal income tax on the withdrawal, making it function exactly like a Traditional IRA. But if you use it for medical expenses in retirement (which you will have plenty of), it remains 100% tax-free.

Part 5: Head-to-Head Comparison: Traditional Health Plans vs. HDHP + HSA

To truly understand which strategy aligns with your life, we must place them side-by-side across the most critical financial vectors.

| Feature / Metric | Traditional Health Plan (Low Deductible PPO/HMO) | HDHP paired with an HSA |

| Primary Purpose | Maximum predictability; transferring immediate financial risk to the insurer. | Long-term wealth building; taking on immediate risk to unlock tax shelters. |

| Monthly Premium Cost | High. You pay a heavy premium for the luxury of low out-of-pocket costs. | Low. The insurer rewards you with cheap premiums for taking on a high deductible. |

| Deductible Burden | Low to Moderate. Often ranges from $500 to $1,500. | High. Often ranges from $3,000 to $7,500+. |

| Copayments | Yes. Flat fees (e.g., $30) for most routine services and prescriptions. | No. You pay the full negotiated rate for services until the massive deductible is met. |

| Tax Advantages | None. Premiums may be pre-tax if through an employer, but there is no wealth-building element. | Massive. The Triple-Tax Advantage on contributions, growth, and medical withdrawals. |

| Rollover / Expiration | N/A. You cannot roll over unused insurance premiums. The money is gone. | Yes. Unused HSA funds roll over forever and compound through investments. |

| Ownership | The policy belongs to the insurer/employer. | The HSA bank account is 100% owned by you. |

| Best Suited For… | The chronically ill, families with small children, and risk-averse budgeters. | Young professionals, the healthy, and aggressive retirement investors. |

Part 6: Pros and Cons Analysis

Every financial product involves a strategic trade-off. Here is the unvarnished reality of both options.

Traditional Health Insurance Plans

The Pros:

- Financial Predictability: You know exactly what a doctor’s visit will cost ($30 copay). This makes creating a monthly household budget incredibly easy.

- Immediate Comprehensive Coverage: You do not have to drain your savings account by paying $3,000 out-of-pocket before the insurance company steps in to help with a broken arm.

- Better for Chronic Conditions: If you require expensive daily medications (like insulin) or frequent specialist visits, a traditional plan absorbs these high costs immediately via manageable copays.

The Cons:

- A Massive Sunk Cost: You will pay thousands of dollars in high premiums every year. If you are perfectly healthy and never visit the doctor, that money is completely gone. You receive zero return on investment.

- Less Consumer Control: Because the copay is so low, consumers rarely check the actual price of medical services, leading to system-wide healthcare inflation.

- No Tax-Sheltered Savings: You have no vehicle to save tax-free money for future healthcare costs in retirement.

HDHP + Health Savings Account (HSA)

The Pros:

- Lower Monthly Overhead: HDHP premiums are significantly cheaper. You keep more of your paycheck every month.

- Unrivaled Tax Mitigation: The HSA is a legal tax haven. Maximizing it reduces your taxable income, saving you thousands in IRS obligations.

- Generational Wealth Building: Investing your HSA funds in the stock market turns your healthcare account into a massive, compounding retirement asset that can eventually be passed down to your spouse tax-free.

- Employer Free Money: Many employers actively deposit “seed money” (e.g., $500 to $1,000 a year) directly into your HSA just for choosing the HDHP option, effectively lowering your true deductible.

The Cons:

- The High Upfront Cash Requirement: If you get into a major car accident in January before you have had time to build up your HSA balance, you are personally on the hook for a massive $4,000+ deductible out of your own pocket.

- Discourages Necessary Care: Studies show that some people with HDHPs avoid going to the doctor when they are sick because they don’t want to pay the high out-of-pocket costs, leading to worse health outcomes down the road.

- Administrative Burden: You have to actively manage your HSA, keep receipts to prove purchases were for “qualified medical expenses,” and actively choose your stock market investments.

Part 7: Real-World Scenario: The Cost Comparison Math

To truly grasp the impact of this decision, let’s run a real-world mathematical simulation for 2026.

Meet two colleagues, David and Sarah. Both are 30 years old, generally healthy, make $85,000 a year, and only visit the doctor once a year for a minor issue (like a sinus infection). They are choosing their employer benefits for the year.

David chooses the Traditional PPO Plan:

- Monthly Premium: $300/month ($3,600/year out of his paycheck).

- Deductible: $1,000.

- Doctor Visit Copay: $30.

- David’s Year: He pays his $3,600 in premiums. He gets a sinus infection, goes to the doctor, and pays his $30 copay.

- David’s Total Financial Loss for the Year: $3,630. He has zero dollars saved for the future.

Sarah chooses the HDHP + HSA Strategy:

- Monthly Premium: $100/month ($1,200/year out of her paycheck).

- Deductible: $3,500.

- Doctor Visit Cost: She must pay the full negotiated rate of $150 out of pocket.

- HSA Contribution: Sarah takes the $2,400 she saved on premiums (compared to David) and deposits it into her HSA.

- Sarah’s Year: She pays her $1,200 in premiums. She gets a sinus infection, goes to the doctor, and pays the full $150 bill using her tax-free HSA funds.

- Sarah’s Total Financial Position: She spent $1,350 total. But more importantly, her $2,400 HSA contribution reduced her taxable income, saving her roughly $500 in income taxes. Her HSA account now has $2,250 left in it, which rolls over to next year and begins earning stock market returns.

- The Winner: By taking on the risk of a higher deductible, Sarah effectively made herself over $2,700 wealthier than David in a single year.

Part 8: Strategic Blueprint: Which Option is Better for You in 2026?

There is no universal “correct” answer in healthcare. The optimal choice is entirely dependent on your historical medical utilization, your cash flow, and your risk tolerance. Use this matrix to make your decision.

You Should Choose a Traditional Health Plan If:

- You Have a Chronic Illness: If you have diabetes, severe asthma, multiple sclerosis, or require expensive, ongoing monthly prescriptions, an HDHP will drain your bank account by February. A traditional plan with predictable copays will save you thousands.

- You Are Planning to Expand Your Family: Pregnancy, labor, and delivery are incredibly expensive. The frequent OBGYN visits and hospital facility fees will instantly max out an HDHP deductible. A traditional plan offers massive savings during a maternity year.

- You Have Small Children: Toddlers are notorious for breaking bones, getting ear infections, and requiring frequent urgent care visits. The predictable copays of a traditional PPO prevent these frequent visits from destroying your monthly budget.

- You Live Paycheck-to-Paycheck: If a sudden $3,000 medical bill would force you into credit card debt or eviction, you cannot afford the risk of an HDHP. Pay the higher monthly premium for the safety of a low deductible.

You Should Choose an HDHP + HSA If:

- You Are Young and Generally Healthy: If your medical history consists of nothing more than an annual physical (which is 100% free anyway) and occasional seasonal allergies, you are throwing money into a furnace by paying for a high-premium traditional plan.

- You Have Robust Emergency Savings: If you have $5,000 sitting comfortably in a high-yield savings account, you can effortlessly absorb the risk of the high deductible in a worst-case scenario. Take the cheap premiums and open the HSA.

- You Are an Aggressive Investor/FIRE Adherent: If you are pursuing the Financial Independence, Retire Early (FIRE) movement, the HSA is your greatest weapon. Maxing it out every year and investing it in index funds will create a massive, tax-free medical war chest for your retirement years when you will actually need it.

- You Are in a High Tax Bracket: High-income earners desperately need legal tax shelters. The tax deductions generated by maxing out an HSA ($8,550 for a family in 2026) are too lucrative for a high-earner to pass up.

Part 9: 4 Costly Mistakes to Avoid During Open Enrollment

Even if you choose the right overall strategy, administrative errors can destroy your financial efficiency. Avoid these critical blunders:

- Choosing Based Only on the Premium: Never select a plan solely because the monthly cost is low. You must calculate your Estimated Total Annual Cost (12 months of premiums + your expected out-of-pocket costs based on last year’s medical usage).

- Using Your HSA as a Checking Account: The biggest mistake HDHP users make is spending their HSA funds on minor expenses like a $15 bottle of Tylenol. To harness the true power of the HSA, you must invest the funds and let them grow. Pay for small medical expenses out of your regular checking account if you can afford it.

- Ignoring the Prescription Formulary: Before signing up for any plan, verify that your specific daily medications are covered. A traditional plan is useless if it classifies your life-saving medication as a “Tier 4 Specialty Drug” requiring 50% coinsurance.

- Forgetting the HSA Contribution Deadline: You actually have until Tax Day (usually April 15th of the following year) to max out your HSA contributions for the previous calendar year. If you have extra cash in March, dump it into your HSA to lower your tax bill before you file.

Part 10: Frequently Asked Questions (FAQ)

Can I open an HSA on my own if I don’t have health insurance?

No. Federal law strictly mandates that you must be actively enrolled in a qualifying High-Deductible Health Plan (HDHP) on the first day of the month to contribute to an HSA. If you drop your HDHP, you can still spend the money already in your HSA, but you cannot legally make any new contributions.

If I switch to a traditional PPO next year, do I lose my HSA funds?

Absolutely not. You own the HSA account forever. If you switch from an HDHP to a traditional PPO next year (perhaps because you are having a baby), you can no longer deposit new money into the HSA. However, the existing funds remain yours to invest, grow, and spend tax-free on medical expenses.

Can I use my HSA funds to pay for my spouse and children’s medical bills?

Yes. You can use your tax-free HSA funds to pay for the qualified medical expenses of yourself, your spouse, and any tax dependents claimed on your IRS tax return—even if those family members are covered under a completely different, non-HDHP health insurance policy.

What happens to my HSA if I die?

If you name your spouse as the designated beneficiary, the HSA transfers to them seamlessly and becomes their own HSA, maintaining all tax-free benefits. If you name anyone other than your spouse (like a child or a trust), the account immediately loses its HSA status, and the fair market value of the account becomes fully taxable income to the beneficiary in the year of your death.

Are HSA funds “Use it or Lose it” like an FSA?

No. This is the most common and dangerous misconception. Flexible Spending Accounts (FSAs) expire at the end of the year. Health Savings Accounts (HSAs) roll over indefinitely and never expire.

Conclusion: Aligning Coverage with Your Future

In 2026, the debate between traditional health insurance plans and Health Savings Accounts is not about finding a single, universally superior option. It is an exercise in profound self-awareness, requiring you to align your medical realities with your long-term wealth-building goals.

Traditional health insurance plans—whether PPO, HMO, or EPO—offer an invaluable psychological and financial safety net. They provide ultimate predictability, ensuring that those with chronic conditions or growing families can access premium medical care without the constant fear of draining their bank accounts.

Conversely, the High-Deductible Health Plan paired with an HSA represents a paradigm shift in personal finance. It rewards healthy, financially disciplined individuals by transforming their healthcare overhead into the most aggressive, triple-tax-advantaged wealth-building vehicle available in the American tax code.

To win the healthcare game, you must stop viewing insurance merely as a monthly bill to be paid. Treat it as a foundational pillar of your holistic financial portfolio. Assess your medical history ruthlessly, calculate your total annual risk exposure, and confidently select the strategy that protects your physical health today while securing your financial independence tomorrow.

Sources

- Healthcare.gov – High-Deductible Health Plans and HSAs

- IRS – Health Savings Accounts and Other Tax-Favored Health Plans