Life insurance provides financial protection for your loved ones, but many policies can be customized to better meet your specific needs. This customization is often achieved through riders, which are optional additions that expand or modify the benefits of a life insurance policy.

Understanding life insurance riders explained in simple terms can help you decide whether these additional features are worth the extra cost. Some riders provide financial support during serious illness, while others offer protection for family members or allow future coverage increases.

This guide covers life insurance riders explained in detail, including the most common rider types, benefits, costs, and situations where riders may be valuable.

What Are Life Insurance Riders?

Life insurance riders are optional policy provisions that can be added to a life insurance contract.

These additions provide extra benefits beyond the standard death benefit included in a policy.

Depending on the insurer, riders may be available when purchasing a policy or added later under certain conditions.

Common reasons for adding riders include:

- Increased financial protection

- Coverage flexibility

- Family security

- Protection against future health risks

- Access to benefits during serious illness

Understanding life insurance riders explained properly can help policyholders make informed decisions about coverage customization.

Life Insurance Riders Explained: Why Riders Matter

Standard life insurance policies primarily focus on providing a death benefit.

However, life circumstances can change over time.

Riders can help address situations such as:

- Disability

- Critical illness

- Long-term care needs

- Child protection

- Income loss

Many families choose riders because they provide additional financial security without requiring separate insurance policies.

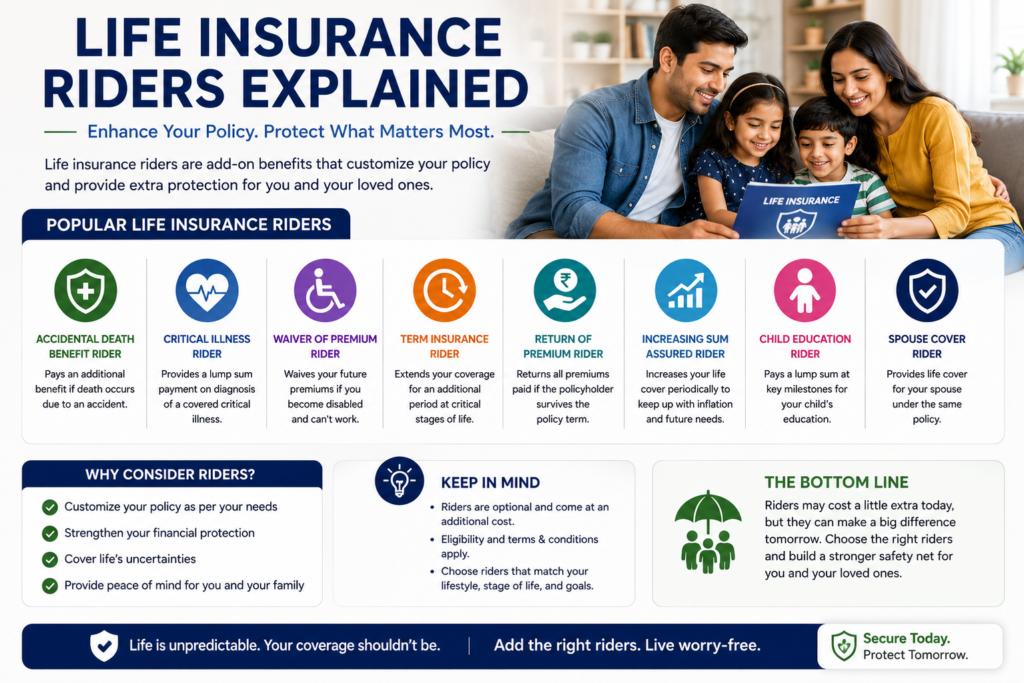

Life Insurance Riders Explained: Common Rider Types

There are several popular rider options available in the life insurance market.

Accelerated Death Benefit Rider

The accelerated death benefit rider allows policyholders to access part of their death benefit while still alive if diagnosed with a qualifying terminal illness.

Benefits include:

- Medical expense support

- Reduced financial stress

- Access to funds during treatment

This is one of the most commonly selected riders.

Waiver of Premium Rider

A waiver of premium rider allows policyholders to stop paying premiums if they become disabled and unable to work.

Advantages include:

- Maintains coverage

- Prevents policy lapse

- Protects long-term benefits

Many younger policyholders consider this rider valuable.

Child Term Rider

A child term rider provides life insurance coverage for children under a parent’s policy.

Benefits include:

- Affordable coverage

- Coverage for multiple children

- Future conversion opportunities

Many families appreciate the convenience of this rider.

Spouse Rider

A spouse rider extends limited life insurance protection to a spouse under the same policy.

Advantages include:

- Simplified policy management

- Cost-effective coverage

- Additional family protection

This rider can be useful for families seeking affordable coverage options.

Life Insurance Riders Explained: Guaranteed Insurability Rider

A guaranteed insurability rider allows policyholders to increase coverage in the future without undergoing another medical examination.

This rider may be valuable when:

- Getting married

- Having children

- Purchasing a home

- Increasing financial responsibilities

Future health changes do not affect eligibility when this rider is used according to policy terms.

Life Insurance Riders Explained: Accidental Death Benefit Rider

An accidental death benefit rider provides an additional payout if death results from a qualifying accident.

This rider is sometimes referred to as “double indemnity” coverage.

Potential benefits include:

- Increased financial protection

- Additional support for beneficiaries

- Enhanced coverage during working years

However, coverage limitations often apply.

Life Insurance Riders Explained: Long-Term Care Rider

Long-term care expenses can be significant during retirement.

A long-term care rider allows policyholders to access part of their life insurance benefits to help pay for:

- Nursing home care

- Assisted living facilities

- Home healthcare services

Many consumers view this rider as a valuable planning tool.

Life Insurance Riders Explained: Critical Illness Rider

Critical illness riders provide financial support after diagnosis of specific serious medical conditions.

Examples may include:

- Heart attack

- Stroke

- Certain cancers

Benefits may be used for:

- Medical bills

- Recovery expenses

- Household costs

- Income replacement

Coverage terms vary by insurer.

Benefits of Life Insurance Riders

Understanding life insurance riders explained also requires evaluating their advantages.

Greater Coverage Flexibility

Riders allow policies to adapt to changing life circumstances.

Additional Financial Protection

Certain riders provide protection against disability, illness, or unexpected life events.

Family Security

Family-focused riders can enhance protection for spouses and children.

Convenience

Adding riders is often easier than purchasing separate insurance products.

Potential Drawbacks of Life Insurance Riders

While riders provide benefits, they also have disadvantages.

Increased Premium Costs

Many riders require additional premium payments.

Coverage Restrictions

Some riders include eligibility requirements and exclusions.

Complexity

Multiple riders can make policies more difficult to understand.

Limited Availability

Not all insurers offer every rider type.

Who Should Consider Life Insurance Riders?

Life insurance riders may be particularly valuable for:

Parents

Families with children often benefit from additional protection options.

Homeowners

Large financial obligations may justify expanded coverage.

Individuals With Dependents

Dependents often rely on continued financial support.

Young Adults

Younger applicants may secure riders at lower costs.

How Much Do Life Insurance Riders Cost?

Rider costs vary based on:

- Rider type

- Age

- Health status

- Coverage amount

- Insurance provider

Some riders add only a small amount to monthly premiums, while others may significantly increase costs.

Comparing costs and benefits is essential before making a decision.

Life Insurance Riders Explained: Comparison Table

| Rider Type | Main Benefit | Typical Use |

|---|---|---|

| Accelerated Death Benefit | Early access to benefits | Terminal illness |

| Waiver of Premium | Premium relief | Disability |

| Child Term Rider | Child coverage | Family protection |

| Spouse Rider | Spouse coverage | Family planning |

| Guaranteed Insurability | Future coverage increases | Major life events |

| Accidental Death Rider | Additional payout | Accident protection |

| Long-Term Care Rider | Care expenses | Retirement planning |

| Critical Illness Rider | Medical support | Serious illness |

Common Mistakes When Choosing Riders

Adding Too Many Riders

Not every rider is necessary for every policyholder.

Ignoring Costs

Additional benefits should justify premium increases.

Failing to Review Policy Terms

Coverage limitations vary significantly.

Choosing Riders Without Assessing Needs

Coverage decisions should align with personal financial goals.

Frequently Asked Questions About Life Insurance Riders Explained

Are life insurance riders worth it?

Many riders provide valuable protection, but suitability depends on individual circumstances.

Which life insurance rider is most popular?

Accelerated death benefit riders are among the most commonly selected options.

Can riders be added later?

Some riders may be added after policy purchase, depending on insurer rules.

Do riders increase premiums?

Many riders increase premiums, although some may be included at no extra cost.

Should young families consider riders?

Many young families benefit from riders that provide flexibility and additional protection.

Conclusion

Understanding life insurance riders explained in simple terms helps consumers make smarter insurance decisions. Riders can enhance a standard life insurance policy by providing additional protection for disability, critical illness, family members, and future life changes.

Before adding riders, carefully evaluate your financial goals, family needs, and budget. Choosing the right riders can improve your overall coverage while providing greater peace of mind for you and your loved ones. National Association of Insurance Commissioners (NAIC)