Choosing the right health insurance plan can significantly impact your healthcare costs and access to medical services. Among the most common health insurance options available today are PPO and HMO health plans. While both provide valuable healthcare coverage, they differ in terms of flexibility, provider networks, costs, and referral requirements.

Understanding the differences between PPO vs HMO health plans can help individuals and families make informed decisions about their healthcare coverage. This guide explains how each plan works, their advantages and disadvantages, and which option may be the best fit for your needs in 2026.

Table of Contents

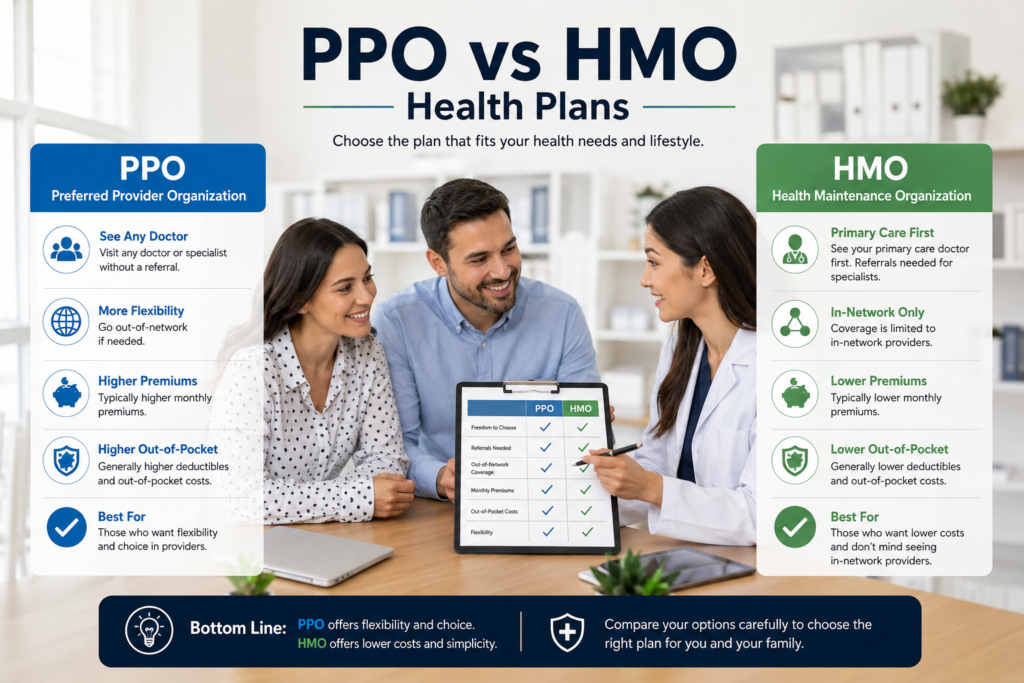

PPO vs HMO Health Plans: Understanding the Key Differences

A Health Maintenance Organization (HMO) plan is a type of health insurance that provides coverage through a specific network of healthcare providers.

Members are generally required to select a primary care physician (PCP) who coordinates their healthcare services and provides referrals to specialists when necessary.

HMO plans focus on preventive care and coordinated treatment, helping to reduce healthcare costs while maintaining quality care.

Key Features of HMO Plans

- Lower monthly premiums

- Lower out-of-pocket costs

- Required primary care physician

- Specialist referrals required

- Limited provider network

- Little or no out-of-network coverage

What Is a PPO Health Plan?

A Preferred Provider Organization (PPO) plan offers greater flexibility when choosing healthcare providers.

Unlike HMO plans, PPO members are not required to choose a primary care physician and can typically see specialists without obtaining referrals.

PPO plans also provide coverage for out-of-network care, although costs are usually higher compared to in-network services.

Key Features of PPO Plans

- Larger provider network

- No specialist referrals required

- Greater provider flexibility

- Out-of-network coverage available

- Higher monthly premiums

- Higher deductibles

PPO vs HMO: Major Differences

Although both plan types provide health insurance coverage, they operate differently.

| Feature | HMO | PPO |

|---|---|---|

| Monthly Premium | Lower | Higher |

| Deductible | Lower | Higher |

| Primary Care Physician | Required | Not Required |

| Specialist Referrals | Required | Not Required |

| Provider Flexibility | Limited | High |

| Out-of-Network Coverage | Usually No | Yes |

| Administrative Simplicity | High | Moderate |

PPO vs HMO Health Plans Provider Networks

One of the biggest differences between PPO and HMO plans involves provider networks.

HMO Networks

HMO plans require members to receive healthcare services from providers within the plan’s approved network.

If a member visits an out-of-network provider, coverage is generally not available except during emergencies.

This restriction helps insurers negotiate lower healthcare costs.

PPO Networks

PPO plans offer access to larger provider networks.

Members may visit both in-network and out-of-network providers.

While out-of-network services are covered, patients usually pay more for these visits.

For individuals who frequently travel or prefer flexibility, PPO plans may provide significant advantages.

PPO vs HMO Health Plans Cost Comparison

Cost is often a major factor when selecting health insurance.

HMO Cost Advantages

HMO plans are typically less expensive because:

- Smaller provider networks reduce costs.

- Coordinated care minimizes unnecessary services.

- Preventive healthcare is strongly encouraged.

Typical HMO benefits include:

- Lower monthly premiums

- Lower deductibles

- Lower copayments

- Lower annual healthcare expenses

PPO Cost Considerations

PPO plans generally cost more because they provide greater flexibility.

Policyholders often pay:

- Higher monthly premiums

- Higher deductibles

- Higher coinsurance

- Increased out-of-pocket expenses

However, the additional flexibility can be valuable for many individuals.

Primary Care Physicians and Referrals

How HMO Referrals Work

In an HMO plan, the primary care physician serves as the central point of care.

When specialized treatment is needed, the PCP issues referrals to approved specialists.

This coordinated approach helps manage healthcare expenses while ensuring continuity of care.

PPO Referral Freedom

PPO plans eliminate the referral requirement.

Patients can schedule appointments directly with specialists without obtaining prior authorization from a primary care physician.

This flexibility can save time and simplify healthcare decisions.

Preventive Care Benefits

Both PPO and HMO plans generally emphasize preventive healthcare.

Preventive services may include:

- Annual physical exams

- Vaccinations

- Health screenings

- Wellness visits

- Preventive counseling

Early detection of medical conditions often reduces long-term healthcare expenses.

Who Should Choose an HMO Plan?

An HMO plan may be a good option for individuals who:

Want Lower Costs

Budget-conscious families often appreciate lower premiums and predictable healthcare expenses.

Prefer Coordinated Care

Patients who value having a primary care physician manage their healthcare may benefit from an HMO.

Rarely Travel

Individuals who typically receive care near home may not need broader provider access.

Do Not Require Frequent Specialists

People with generally good health may find HMO coverage sufficient for their needs.

Who Should Choose a PPO Plan?

A PPO plan may be more suitable for individuals who:

Want Greater Flexibility

Those who prefer choosing providers without restrictions often prefer PPO plans.

Travel Frequently

PPO plans can provide broader coverage when traveling or relocating temporarily.

Need Specialist Care

Individuals managing chronic conditions may benefit from direct specialist access.

Have Preferred Doctors

Patients who wish to continue seeing specific providers often find PPO plans advantageous.

Advantages of HMO Plans

Lower Monthly Premiums

One of the most appealing benefits of HMO plans is affordability.

Lower Deductibles

Many HMO plans feature lower deductibles than PPO alternatives.

Simplified Care Management

Primary care physicians coordinate treatments, reducing confusion and duplication.

Strong Preventive Focus

Routine healthcare services help maintain long-term health.

Advantages of PPO Plans

Greater Provider Choice

Patients have more freedom when selecting doctors and specialists.

No Referral Requirements

Specialist appointments can be scheduled directly.

Out-of-Network Coverage

Coverage remains available even when visiting providers outside the network.

Flexibility During Travel

Frequent travelers benefit from broader access to healthcare providers.

Potential Drawbacks of HMO Plans

While HMO plans are affordable, they also have limitations.

Common disadvantages include:

- Limited provider choices

- Referral requirements

- Minimal out-of-network coverage

- Less flexibility

Potential Drawbacks of PPO Plans

PPO plans provide flexibility but come with trade-offs.

Potential disadvantages include:

- Higher premiums

- Higher deductibles

- Increased healthcare expenses

- More complex billing

Common Mistakes When Choosing a Health Plan

Many consumers make mistakes when comparing PPO and HMO plans.

Focusing Only on Premiums

Lower premiums do not always mean lower overall costs.

Ignoring Provider Networks

Patients should confirm that preferred doctors participate in the network.

Overlooking Prescription Coverage

Medication coverage can significantly affect total healthcare expenses.

Not Evaluating Healthcare Usage

Families should consider how often they use healthcare services before selecting a plan.

Frequently Asked Questions About PPO vs HMO Health Plans

Is PPO better than HMO?

Neither plan is universally better. The right choice depends on healthcare needs, budget, and provider preferences.

Why are PPO plans more expensive?

PPO plans offer greater flexibility, larger provider networks, and out-of-network coverage.

Do HMO plans cover emergencies?

Yes. Emergency medical services are generally covered regardless of network restrictions.

Can I switch from an HMO to a PPO?

Yes. Many individuals switch plans during open enrollment periods or after qualifying life events.

Which plan is best for families?

Families seeking lower costs may prefer HMO plans, while those wanting flexibility may choose PPO plans.

Conclusion

When comparing PPO vs HMO health plans, the best option depends on your healthcare needs, budget, and preferred level of flexibility.

HMO plans provide affordable, coordinated care with lower costs, making them attractive for many families. PPO plans offer greater provider choice and flexibility, which may be valuable for individuals with complex healthcare needs or frequent travel requirements.

Carefully reviewing provider networks, costs, benefits, and healthcare usage patterns will help you choose the right health insurance plan in 2026.

Pingback: Family Health Insurance Complete Guide 2026: Coverage, Costs & Benefits

Pingback: Best Life Insurance for Young Families in 2026: Complete Buying Guide

Pingback: How to Choose a Health Insurance Plan in 2026: Complete Beginner's Guide

Pingback: Life Insurance Riders Explained: Complete Guide to Optional Coverage in 2026

Pingback: What Does Home Insurance Cover? Complete Homeowners Insurance Guide for 2026

Pingback: Home Insurance Coverage Explained: Complete Homeowners Guide for 2026

Pingback: Small Business Insurance Checklist: Essential Coverage Guide for 2026