Health insurance can be confusing, especially when you encounter terms like deductibles, copays, coinsurance, and out-of-pocket maximums. Among these terms, health insurance deductibles and copays are two of the most important factors affecting how much you pay for healthcare services.

Understanding health insurance deductibles and copays can help you compare plans, manage healthcare costs, and avoid unexpected medical bills. Whether you are purchasing insurance for yourself or your family, learning how these cost-sharing features work is essential for making informed healthcare decisions.

Table of Contents

What Are Health Insurance Deductibles and Copays?

Health insurance deductibles and copays are cost-sharing mechanisms that determine how medical expenses are divided between you and your insurance company.

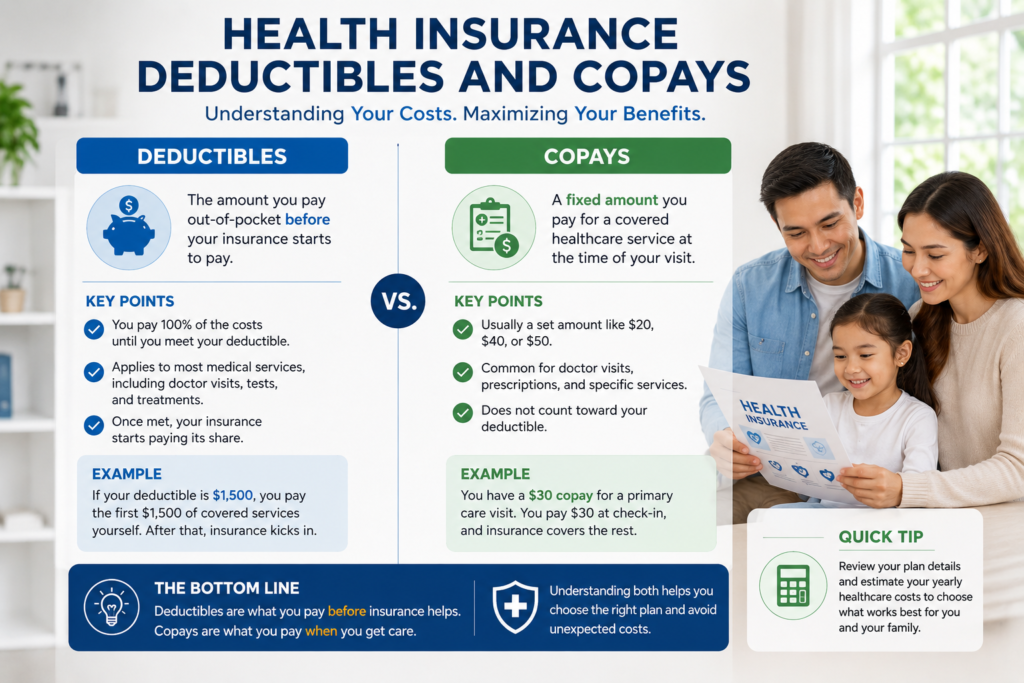

A deductible is the amount you must pay out of pocket before your insurance starts covering eligible healthcare services.

A copay is a fixed amount you pay for a covered healthcare service, such as a doctor visit or prescription medication.

Although both contribute to healthcare expenses, they function differently within your insurance plan.

Understanding Health Insurance Deductibles and Copays

To fully understand health insurance deductibles and copays, it is important to examine each component separately.

What Is a Health Insurance Deductible?

A deductible is the amount you must pay for covered medical services before your insurance provider begins sharing costs.

For example:

- Annual deductible: $2,000

- Medical expenses incurred: $2,000

- Insurance contribution before deductible: $0

Once the deductible is met, your insurer begins covering eligible expenses according to the plan terms.

What Is a Copay?

A copay is a predetermined fixed fee that you pay when receiving certain healthcare services.

Examples include:

- Primary care visit: $25 copay

- Specialist visit: $50 copay

- Prescription medication: $15 copay

Unlike deductibles, copays are usually paid at the time of service.

Health Insurance Deductibles and Copays: Key Differences

Many consumers confuse deductibles and copays because both involve out-of-pocket spending.

| Feature | Deductible | Copay |

|---|---|---|

| Payment Type | Annual spending requirement | Fixed fee per service |

| When Paid | Before insurance coverage begins | During healthcare visits |

| Amount | Often hundreds or thousands of dollars | Usually $10–$100 |

| Frequency | Until deductible is met | Every qualifying visit |

| Purpose | Cost-sharing threshold | Routine service payment |

Understanding these distinctions is crucial when comparing health insurance deductibles and copays across different plans.

How Health Insurance Deductibles and Copays Work Together

Many health insurance plans use both deductibles and copays simultaneously.

For example:

A patient has:

- $1,500 deductible

- $30 primary care copay

The patient visits a doctor and pays the $30 copay.

Later, they undergo a medical procedure costing $1,200. Since the deductible has not yet been met, the patient pays the procedure costs until reaching the deductible threshold.

Once the deductible is satisfied, insurance coverage begins according to plan terms.

Why Health Insurance Deductibles and Copays Matter

Health insurance deductibles and copays directly affect your healthcare budget.

Impact on Monthly Premiums

Plans with higher deductibles often have lower monthly premiums.

Plans with lower deductibles typically have higher monthly premiums.

Impact on Healthcare Spending

If you frequently visit healthcare providers, lower deductibles and copays may reduce annual healthcare costs.

Impact on Financial Planning

Understanding health insurance deductibles and copays helps families budget for potential medical expenses throughout the year.

High-Deductible vs Low-Deductible Health Plans

Many insurance shoppers compare high-deductible and low-deductible plans.

High-Deductible Health Plans

Advantages:

- Lower monthly premiums

- Potential eligibility for Health Savings Accounts (HSAs)

- Good for healthy individuals

Disadvantages:

- Higher upfront healthcare expenses

- Greater financial responsibility during emergencies

Low-Deductible Health Plans

Advantages:

- Lower out-of-pocket costs when receiving care

- More predictable healthcare spending

Disadvantages:

- Higher monthly premiums

- Increased ongoing insurance costs

Common Copay Structures

Insurance companies often assign different copays to different services.

Typical examples include:

| Healthcare Service | Typical Copay |

| Primary Care Visit | $20-$40 |

| Specialist Visit | $40-$80 |

| Urgent Care | $50-$100 |

| Emergency Room | $100-$500 |

| Generic Prescription | $10-$25 |

The exact amounts vary by insurer and policy.

Health Insurance Deductibles and Copays for Families

Families often face different healthcare needs than individuals.

When evaluating health insurance deductibles and copays, families should consider:

- Number of family members covered

- Frequency of doctor visits

- Ongoing prescriptions

- Planned medical procedures

- Children’s healthcare needs

Family plans may include both individual deductibles and family deductibles.

Health Insurance Deductibles and Copays in PPO Plans

PPO plans often feature:

- Higher premiums

- Higher deductibles

- Flexible provider choices

- Out-of-network coverage

Because PPO plans provide greater freedom, deductibles are often higher than HMO plans.

Health Insurance Deductibles and Copays in HMO Plans

HMO plans generally include:

- Lower premiums

- Lower deductibles

- Lower copays

- Coordinated healthcare services

Many families appreciate the affordability offered by HMO plans.

Tips for Choosing the Right Deductible and Copay Structure

Evaluate Healthcare Usage

Consider how frequently you use healthcare services.

Review Emergency Savings

High-deductible plans require greater financial preparedness.

Consider Family Size

Larger families often benefit from lower deductibles.

Compare Total Costs

Do not focus solely on premiums.

Analyze:

- Premiums

- Deductibles

- Copays

- Coinsurance

- Out-of-pocket maximums

Common Mistakes When Comparing Health Insurance Deductibles and Copays

Ignoring Annual Healthcare Usage

Healthcare needs vary from person to person.

Choosing the Lowest Premium

Low premiums may result in significantly higher deductibles.

Overlooking Specialist Costs

Frequent specialist visits can increase overall expenses.

Failing to Read Plan Details

Coverage rules vary considerably between insurance providers.

Frequently Asked Questions About Health Insurance Deductibles and Copays

Do I pay a copay before meeting my deductible?

In many plans, yes. Certain services require copays regardless of deductible status.

Is a higher deductible always better?

Not necessarily. It depends on your healthcare usage and financial situation.

Do family plans have separate deductibles?

Many family plans include both individual and family deductible limits.

Can copays count toward deductibles?

Some plans allow this, while others do not. Always review plan details.

What is more important, deductible or copay?

Both matter. The right balance depends on how frequently you use healthcare services.

Conclusion

Understanding health insurance deductibles and copays is essential for managing healthcare expenses and selecting the right insurance plan. These two cost-sharing features directly affect how much you pay for medical care throughout the year.

By comparing deductibles, copays, premiums, and provider networks, individuals and families can make smarter insurance decisions. Carefully reviewing health insurance deductibles and copays before enrolling in a plan can help reduce financial stress while ensuring access to quality healthcare when it is needed most.

Pingback: Life Insurance Riders Explained: Complete Guide to Optional Coverage in 2026

Pingback: What Does Home Insurance Cover? Complete Homeowners Insurance Guide for 2026

Pingback: How Much Home Insurance Do You Need in 2026? Complete Coverage Guide

Pingback: Small Business Insurance Checklist: Essential Coverage Guide for 2026