One of the most common questions people ask when shopping for life insurance is: how much life insurance do you need? Buying too little coverage may leave your loved ones financially vulnerable, while purchasing too much coverage can result in unnecessarily high premiums.

The right amount of life insurance depends on several factors, including your income, debts, family size, future expenses, and long-term financial goals. Understanding how much life insurance you need can help ensure your family remains financially secure if the unexpected happens.

This guide explains how much life insurance you need, how coverage amounts are calculated, and the key factors to consider when selecting a policy in 2026.

Why Understanding How Much Life Insurance Do You Need Is Important

Life insurance is designed to replace income and provide financial support to your beneficiaries after your death.

Without adequate coverage, your family may struggle to pay for:

- Mortgage payments

- Household expenses

- Childcare costs

- Education expenses

- Existing debts

- Funeral costs

- Future living expenses

Learning how much life insurance you need helps ensure that your loved ones are protected from financial hardship.

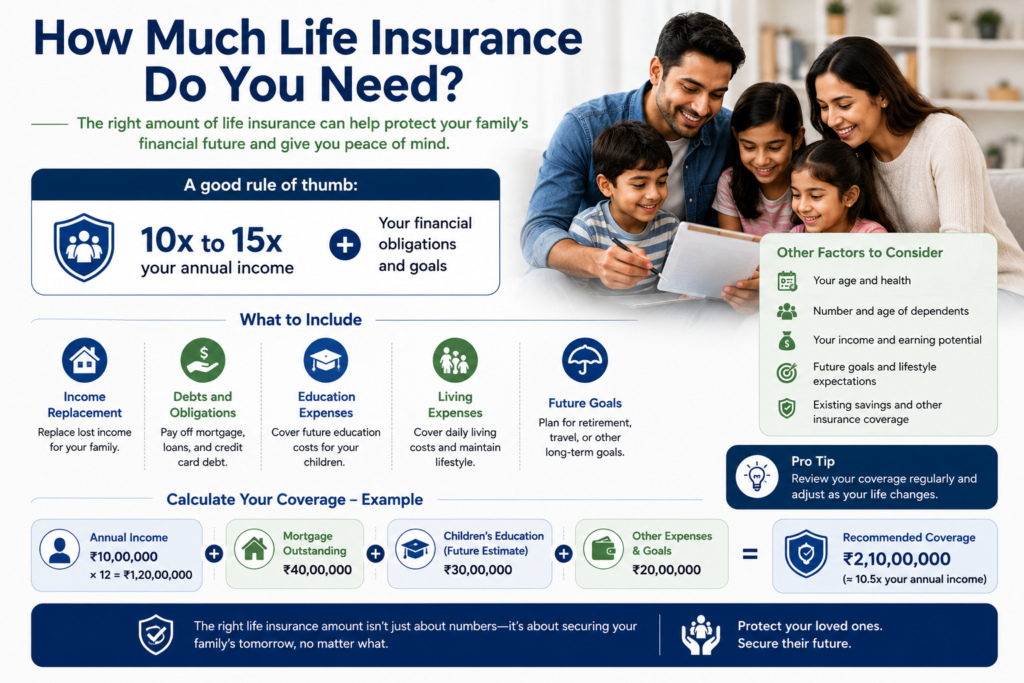

How Much Life Insurance Do You Need? The Basic Rule

A common rule used by financial professionals is to purchase coverage equal to 10 to 15 times your annual income.

For example:

| Annual Income | Recommended Coverage |

|---|---|

| $50,000 | $500,000 – $750,000 |

| $75,000 | $750,000 – $1,125,000 |

| $100,000 | $1,000,000 – $1,500,000 |

| $150,000 | $1,500,000 – $2,250,000 |

While this rule provides a useful starting point, individual circumstances often require a more personalized calculation.

How Much Life Insurance Do You Need Based on Income Replacement?

Income replacement is one of the most important factors when determining coverage.

Ask yourself:

- How many years would your family need financial support?

- How much income would need to be replaced?

- Would surviving family members continue working?

For example:

- Annual income: $80,000

- Desired replacement period: 15 years

Required coverage:

$80,000 × 15 = $1,200,000

This simple approach helps estimate how much life insurance you need to maintain your family’s lifestyle.

How Much Life Insurance Do You Need for Debt Protection?

Outstanding debts should be included in your life insurance calculations.

Common debts include:

- Mortgage balances

- Car loans

- Student loans

- Credit card balances

- Personal loans

Example:

| Debt Type | Amount |

| Mortgage | $250,000 |

| Auto Loan | $20,000 |

| Credit Cards | $10,000 |

| Student Loans | $20,000 |

| Total Debt | $300,000 |

Life insurance can help ensure these obligations do not become a burden on surviving family members.

How Much Life Insurance Do You Need for Children?

Parents often purchase life insurance to protect their children’s future.

Potential expenses include:

Childcare Costs

Childcare expenses can be significant, especially for young children.

Education Expenses

Many parents want coverage that can help pay for:

- Private school tuition

- College education

- Vocational training

- Higher education expenses

Daily Living Expenses

Food, clothing, transportation, and healthcare costs should also be considered.

Families with young children often require higher life insurance coverage amounts.

How Much Life Insurance Do You Need If You Have a Mortgage?

For many households, a mortgage represents the largest financial obligation.

If one parent passes away, surviving family members may struggle to continue mortgage payments.

Many financial advisors recommend including the full mortgage balance in your life insurance calculation.

Example:

- Mortgage balance: $350,000

Additional life insurance coverage needed:

$350,000

This helps ensure the family can remain in their home without financial stress.

How Much Life Insurance Do You Need Using the DIME Method?

The DIME method is a popular life insurance calculation strategy.

DIME stands for:

Debt

Outstanding loans and liabilities.

Income

Income replacement for dependents.

Mortgage

Remaining mortgage obligations.

Education

Future educational costs for children.

Example:

| Category | Amount |

| Debt | $50,000 |

| Income Replacement | $1,000,000 |

| Mortgage | $300,000 |

| Education | $100,000 |

| Total Coverage Need | $1,450,000 |

The DIME method provides a comprehensive estimate of how much life insurance you need.

How Much Life Insurance Do You Need If You Are Single?

Single individuals may still benefit from life insurance.

Coverage may help:

- Pay funeral expenses

- Cover personal debts

- Support aging parents

- Leave a financial legacy

Single adults typically require less coverage than families with children.

How Much Life Insurance Do You Need If You Are Married?

Married couples often depend on each other’s income and contributions.

Coverage should account for:

- Shared living expenses

- Debt obligations

- Future retirement plans

- Income replacement needs

Dual-income households may require coverage for both spouses.

How Much Life Insurance Do You Need as a Stay-at-Home Parent?

Many people underestimate the economic value of stay-at-home parents.

Replacing services such as:

- Childcare

- Transportation

- Housekeeping

- Meal preparation

Can cost tens of thousands of dollars annually.

For this reason, stay-at-home parents often benefit from life insurance coverage as well.

Factors That Affect How Much Life Insurance Do You Need

Several factors influence coverage requirements.

Family Size

Larger families often require greater financial protection.

Age

Younger individuals generally need longer coverage periods.

Existing Savings

Substantial savings may reduce insurance needs.

Future Financial Goals

Education funding and retirement planning should be considered.

Health Conditions

Certain health risks may influence policy selection and costs.

Common Mistakes When Determining How Much Life Insurance Do You Need

Choosing Coverage Based Only on Cost

Low premiums may result in insufficient protection.

Ignoring Inflation

Future living costs are likely to increase.

Underestimating Education Expenses

College costs continue to rise.

Forgetting Existing Debts

Outstanding financial obligations should always be included.

Failing to Review Coverage

Life insurance needs change as families grow.

Frequently Asked Questions About How Much Life Insurance Do You Need

How much life insurance do you need if you have children?

Many experts recommend coverage equal to 10–15 times annual income plus future education expenses.

Is $500,000 enough life insurance?

It depends on your income, debts, and family responsibilities.

Should both spouses have life insurance?

In many cases, yes. Both financial and non-financial contributions should be protected.

What happens if I buy too much life insurance?

You may pay higher premiums than necessary.

How often should I review life insurance coverage?

Most experts recommend reviewing coverage every few years or after major life events.

Conclusion

Understanding how much life insurance do you need is one of the most important steps in protecting your family’s financial future. The ideal coverage amount depends on income replacement needs, debts, mortgage obligations, children’s expenses, and long-term financial goals.

By carefully evaluating your situation and using proven calculation methods such as the DIME approach, you can confidently determine how much life insurance you need and select a policy that provides meaningful protection for your loved ones in 2026 and beyond.

Pingback: Best Life Insurance for Young Families in 2026: Complete Buying Guide

Pingback: Family Health Insurance Complete Guide 2026: Coverage, Costs & Benefits

Pingback: How to Choose a Health Insurance Plan in 2026: Complete Beginner's Guide

Pingback: Home Insurance Coverage Explained: Complete Homeowners Guide for 2026

Pingback: What Does Home Insurance Cover? Complete Homeowners Insurance Guide for 2026